Summary of the IPCC AR6 report III

Working Group III

April 2022

The IPCC (Intergovernmental Panel on Climate Change) is an organisation of 195 UN member states whose objective is to regularly assess the most advanced scientific knowledge on climate without bias. It brings together thousands of volunteer experts from around the world to assess, analyse and synthesise the many scientific studies on the subject. IPCC reports are at the heart of international climate negotiations, such as the Paris Agreement (COP21) in 2015 and COP26 in Glasgow in November. In 2007, the IPCC shared the Nobel Peace Prize with Al Gore. The IPCC is organised into three working groups. Group 1 studies the scientific aspects of climate change and produced this report. Group 2 assesses the impacts, vulnerability and adaptation to climate change, and Group 3 studies its mitigation; they will publish their report in 2022.

To download : ipcc_ar6_wgiii_spm.pdf (2.1 MiB)

Introduction

Much has changed since the IPCC’s fifth report in 2012. The Paris Agreement (2015) and the increasing attention paid to climate issues by civil societies and economic actors have put climate objectives more on the agenda. The links between greenhouse gas (GHG) emission trajectories and economic and social development are also better understood. Finally, the continued growth of GHG emissions since 2010 has increased climate risks and severely constrained future trajectories consistent with 1.5°C or 2°C warming.

This summary begins with an update on the current emissions situation, and the trajectories to be followed. It then identifies the various possible levers for action to follow these trajectories. Finally, it draws up a sectoral balance sheet in terms of current emissions, trajectories to be followed, and means of action.

Current GHG emissions and future trajectories

Humans emit several types of GHGs, each with a different atmospheric lifetime and warming power. To compare emissions of different GHGs, they are therefore converted to a common unit - the « CO2 equivalent », denoted CO2-eq, which is, in simplified terms, the amount of CO2 that would cause equivalent warming over a reference period, in this case 100 years.

Overview of current emissions

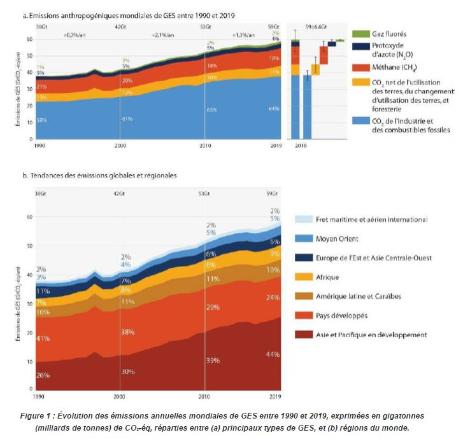

Although annual global GHG emissions have increased at a slower rate since 2010 compared to previous decades, they reached their highest level ever in 2019: 59 GtCO2-eq. This is 12% higher than in 2010, and 54% higher than in 1990. This increase concerns all the main GHGs (Figure 1). In 2019, emissions were split between CO2 from fossil fuels and industry (38 GtCO2-eq), CO2 from agriculture, forestry and other land use (AFAT) (6.6 GtCO2-eq), methane (11 GtCO2-eq, or 18% of the total), nitrous oxide (N2O; 2.7 GtCO2-eq), and fluorinated gases (1.4 GtCO2-eq).

Global disparities

Each human emits an average of 8 tonnes of CO2-eq per year. However, this figure does not reflect the enormous variability in emissions, which is largely related to income inequalities: from 2.6 to 19 tCO2-eq per capita for South Asia and North America, respectively. Emissions are proportionally much higher in developed countries, and within each country, mainly concentrated among the richest inhabitants. Globally, the richest 10% of the population are responsible for about 40% of GHG emissions, about 15 times more per person than the poorest 50%.

Current trends and future trajectories

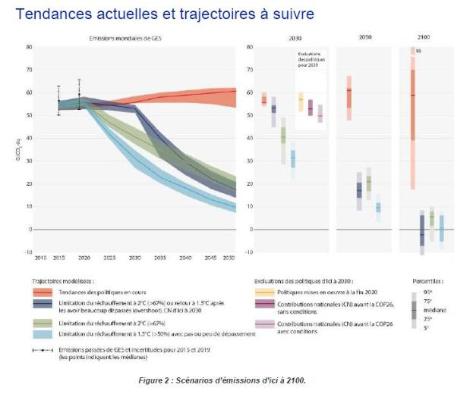

The commitments made by states following the Paris Agreement are not compatible with limiting warming to 1.5°C by 2100 (for which the remaining carbon budget is 500 GtCO2). They even make the objective of staying below +2°C difficult to achieve. Laws adopted before the end of 2020 would lead to a temperature rise of 3.2°C by 2100. Limiting warming to 1.5°C would require emissions to peak before 2025 and then fall by 43% by 2030 compared to 2019, and by 84% by 2050. Such reductions require transforming all economic sectors, and achieving « net zero » CO2 emissions by 2050 (residual emissions offset by carbon capture and storage - CCS). Emissions of other GHGs must also fall sharply. The longer it takes for this to happen, the more CCS will be needed in the second half of the 21st century. However, in all scenarios, the transport, buildings and industry sectors reach net zero later than the energy production and AFAT sectors. Similarly, not all regions of the world will reach net zero at the same time.

Emissions trajectories are not only a function of our future decisions, but also of choices made in the past. On the basis of their current operation, existing fossil fuel infrastructure (e.g. coal-fired power plants) will emit about 660 Gt of CO2-eq during their lifetime, a figure that rises to 850 Gt if planned infrastructure is included. It is therefore clear that some of this infrastructure will have to be abandoned before its planned end of life if we are to have any chance of limiting warming to 1.5°C or even 2°C.

GHG emissions and pandemic

In 2020, the global VOCID-19 pandemic has resulted in a historic 5.8% (or 2 GtCO2) decrease in CO2 emissions from fossil fuel combustion and industry compared to 2019. Despite this decrease, the concentration of GHGs has continued to increase in 2020. Moreover, CO2 emissions started to rise again at the end of 2020.

Main levers for action

Decreasing carbon intensity

Technology development, deployment and transfer can help achieve climate and sustainable development goals. Technology can improve people’s well-being without increasing emissions, environmental impacts and demand for natural resources. Digital technologies, for example, can help make industrial and energy processes more efficient. However, in some sectors, without organised management, technology can also increase energy demand (rebound effect), exacerbate inequalities, concentrate power, increase ethical problems, create unemployment and compromise the well-being of citizens.

At the global level, growth in material consumption, linked to rising incomes, is the main driver of rising GHG emissions, ahead of population growth. The adoption of more energy-efficient technologies and less carbon-intensive means of energy production has reduced the carbon intensity of the economy (i.e. the amount of CO2 emitted per unit of wealth produced), but has not offset the effect of economic growth. Many countries have thus achieved a decoupling between economic growth and emissions, without emitting less GHGs in absolute terms. Only about twenty countries have succeeded in reducing their territorial emissions for at least 10 years, at a rate sufficient to limit global warming to 2°C by 2100. It should be noted, however, that territorial emissions do not take into account emissions linked to imports and exports, particularly those associated with industrial relocation. Thus, part of the territorial emissions of developing countries is due to the production of goods for developed countries. For example, 40% of the carbon footprint of France or Germany comes from their imports.

Role of finance

Finance also has an important role to play in the energy transition. In particular, financial flows must be redirected towards investments that are consistent with climate objectives, as emphasised by the Paris Agreement. This is all the more necessary as developed countries have not met their commitment, made at COP15 in 2009, to finance climate measures in developing countries to the tune of 100 billion dollars per year, which poses problems of confidence in international negotiations.

Investments in adaptation and mitigation have increased by 60% between 2013 and 2020 but are still far below the level needed to limit warming to 2°C. Several economic tools have been developed. Carbon pricing schemes now cover 20% of global CO2 emissions. Green bond and sustainable finance markets have also multiplied, although private actors, who account for 60% of total financing, remain reluctant to invest in areas where economic returns are not guaranteed. In addition, the pandemic has exacerbated inequalities in financial capacity between countries. Harmonising post-Covid stimulus packages and climate targets could potentially address financial needs and reduce bottlenecks. In the short term, this harmonisation would be necessary to meet the targets for financing the needs before 2030, while in the medium term it would reduce the cost to taxpayers.

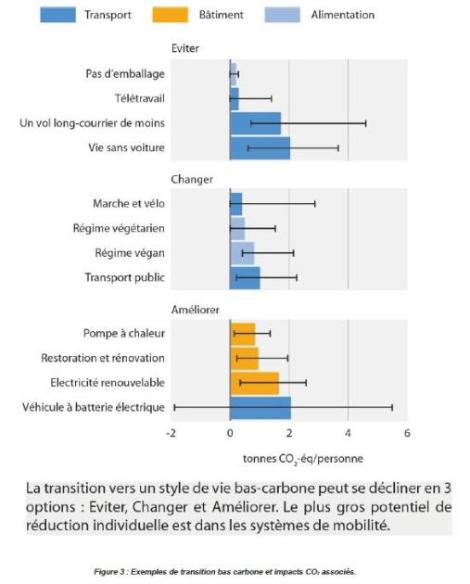

Acting on demand Acting on the demand for goods and services has a significant impact on emissions. A 40-70% reduction in emissions is possible by implementing a large-scale sobriety strategy based on three pillars: ‘avoid’, ‘change’ and ‘improve’ (Figure 3). « Avoidance » has the greatest potential in transport: flying less and minimising car use by adapting infrastructure. « Change » has the most potential in diet, by adopting a plant-based diet. « Improving » has more potential in buildings through the development of passive housing. Such a strategy would also limit the use of carbon capture technologies and the risks associated with land and resource use. Containment during the VOCID-19 pandemic has shown that rapid and large-scale behavioural changes are possible.

Individuals can contribute to sobriety as consumers, citizens, investors and professionals. The most privileged have the capacity to reduce their emissions while setting an example of low-carbon lifestyles: by avoiding air travel, living without a car, switching to electromobility. New social norms could be established if 10-30% of the population changed their behaviour in favour of low-carbon actions. But individual behavioural changes alone will not significantly reduce GHG emissions: action on a collective scale is needed.

Collective scale and international cooperation

Since 2014, climate policy issues are now discussed at multiple levels, from local to national. Non-state actors are increasingly engaged in mitigation: local governments, civil society, businesses and investors, and indigenous peoples. Their actions - from knowledge dissemination and legal action to local experimentation - are having an increasingly significant impact and are helping to change national climate targets. The Paris Agreement is also a turning point in national climate policies. It emphasises ever more ambitious climate targets and the reconciliation of climate mitigation and sustainable development. Many countries have set emission reduction targets, but their legislation is often not up to standard, sometimes even failing to include certain GHGs such as methane.

Development policies must aim to both reduce emissions and encourage sustainable lifestyles. For this to happen, new social norms must be established. For these to be accepted, structural changes in our societies based on principles of equity and social justice are needed, including through economic incentives. Equitable transitions from the local to the international level ensure that the most vulnerable people and communities are not left behind. In addition, increasing the participation of women, minority and marginalised groups amplifies the momentum for climate action. Countries whose economies are mainly based on fossil fuel revenues will be particularly affected by strong GHG mitigation measures. These transition scenarios must therefore take into account the characteristics of each country (context, implementation times, regulatory designs). Studies show that low-carbon energy offers more job opportunities than fossil fuels.

The adaptation and mitigation capacities of developing countries are weaker due to limited economic and institutional resources. International cooperation would thus make it possible to achieve ambitious climate goals through the sharing of financial and technological resources. Some national commitments will not be possible without such support. Partnerships can involve not only states, but also cities, non-governmental organisations and the private sector. Cooperation is all the more important because the institutional and economic barriers are potentially greater than the technological and physical barriers.

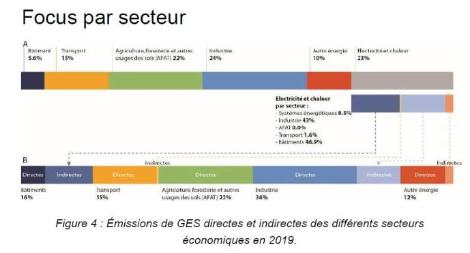

One third of global GHG emissions in 2019 were due to energy production (Figure 4a). But electricity and heat go to other sectors. Thus, after allocating emissions to the sectors consuming this energy, the largest emitter becomes industry with 34% of emissions. AFAT, transport and buildings account for 22%, 15% and 16% respectively. The remaining 12% is due to various losses in the energy system, e.g. gas pipeline leaks.

Energy production

Major changes are needed in this sector: drastic reduction of fossil fuels, use of alternative energies, energy sobriety and efficiency. To limit warming to 1.5°C, the use of coal, oil and gas will have to decrease by 2050 by 95, 60 and 45%, respectively. Continuing to install fossil fuel infrastructure will take up part of the remaining carbon budget.

The share of electricity in the global energy mix is set to increase significantly, from 20% today to around 50% by 2050. Moreover, 95% of electricity will have to be produced by low-carbon technologies in 2050 to stay below 2°C, compared to less than 40% today (including 8% from solar and wind power).

The development of renewable energies, encouraged by public policies and the continuous drop in costs (solar -56%, wind -45%, batteries -64% between 2015 and 2020), has already made it possible to slow the growth of emissions linked to energy production. This relative decarbonisation of the energy production system has been observed in North America, Europe and Eurasia. However, it has not led to an absolute decrease in emissions due to rising global demand.

Transport

The sector accounts for 15% of GHG emissions, and is the one that has increased the most over the last decade (+1.8% per year). Road transport dominates with 70% of emissions, followed by aviation (11%), maritime transport (10%) and rail (1%). The carbon intensity of transport has also increased, mainly due to the rise in aviation emissions (+3.3% per year since 2010) and the deployment of SUVs (40% of sales in 2019).

To limit warming to 1.5°C, the transport sector will have to reduce its emissions by 59% by 2050 (and by 29% to stay below 2°C). To achieve these objectives, it is necessary to put in place demand reduction programmes, improve energy efficiency and adapt infrastructures. For personal travel, this means developing public transport, active transport (cycling, walking, etc.) and shared local mobility (carpooling, car sharing, etc.). Such changes require major work to reorganise urban planning and land use. As for freight (road, air, sea), the reduction of emissions will depend very much on political decisions and technological progress.

As for the carbon intensity of the transport sector, the electrification of light vehicles could be the main factor in reducing GHG emissions by 2050. Improving storage technologies (materials used, energy efficiency and recycling) can reduce the environmental footprint of this electrification. In addition to the new high energy density chemical batteries, other solutions such as hydrogen, biofuels or sustainable synthetic fuels are being added to help reduce the sector’s emissions.

It should also be noted that the adoption of electromobility and the development of public transport and active mobility bring co-benefits through their positive impacts on air quality, health, access to education and gender equality.

Building

Emissions from the sector increased by 50% between 1990 and 2019. They account for 16% of global GHG emissions, including direct emissions (mainly heating) and indirect emissions (due to the production of electricity used in buildings). The sector’s emissions even reach 21% if those linked to the production of construction materials (steel, cement) are included.

There are many ways of reducing emissions in this sector: extending the life of buildings and the materials used to construct them, making housing denser, greening roofs and facades and stepping up efforts to save energy. On this last point, it will be necessary to be vigilant about the overheating of buildings and the increase in air conditioning (+75% between 1990 and 2019).

Finally, many measures to reduce emissions in buildings generate co-benefits. For example, in cities, green roofs and facades, and green spaces increase our capacity to adapt to climate change, helping to combat flooding and heat island effects, and reduce food risks.

Agriculture, Forestry, and Land Use (AFAL)

The AFAT sector currently accounts for 22% of global GHG emissions. It has significant mitigation potential in the short term at relatively low cost. By 2050, it could provide 20-30% of the emission reduction effort needed to limit warming to 2°C. There are many possibilities for reducing emissions: preservation, improved management and restoration of natural areas, sustainable agricultural intensification (agroecology, permaculture, etc.), carbon storage in cultivated soils, CCS, substitution of fossil fuels with bioenergy, reduction of agricultural demand through reduced waste and less meat. Reducing deforestation in tropical regions has the greatest mitigation potential in the sector. Indeed, global deforestation accounts for 45% of total AFAT emissions. Net-zero strategies should encourage the financing of carbon offsetting actions (reforestation, restoration of degraded land…).

Achieving emission reduction targets in the AFAT sector involves overcoming institutional, economic and political constraints, and managing conflicts of use. To achieve the targets in this sector, research and development are essential, as well as the dissemination of technologies, data and know-how. Limited access to these should not be a barrier to the implementation of mitigation measures. The success of policies and measures depends on governance that emphasises integrated land-use planning and management within the framework of the UN Sustainable Development Goals, and supports their implementation.

The reduction of emissions from the AFAT sector is accompanied by co-benefits. For example, reforestation will also benefit biodiversity, increasing ecosystem services. In coastal areas, the preservation of mangroves and wetlands will store carbon, reduce coastal erosion, and limit the effects of rising sea levels. A diet that emits less GHGs also has health benefits. Sustainable management of agricultural land will prevent land degradation and combat food insecurity.

Industry

Industry is the largest emitter of GHGs, accounting for 34% of the global total. Emissions from the production of raw materials can be offset through a combination of electrification of production processes, use of biofuels, carbon capture and storage, and technological efficiency. Manufacturing industry can be largely decarbonised by switching to low-emission fuels, such as hydrogen. Smart demand management and the development of the circular economy will also help reduce the need for raw materials.

Carbon sequestration is necessary to reach net zero in most scenarios limiting warming to 1.5 or 2°C. It relies on two types of solutions: on the one hand, technological solutions: capture and storage of CO2 at source (thermal power plant for example) and direct capture of atmospheric CO2; and on the other hand, natural solutions, presented in the AFAT sector. The sequestration potential is obviously very much linked to the cost of carbon: price estimates vary greatly depending on the capture process.

Achieving net zero in the industry sector will require efforts in governance, relocation and/or training to limit the societal impacts of the measures to be taken.

Never before has humanity emitted as much GHG as it does today. Emissions continue to grow despite the policies implemented, leading us towards a warming of 3.2°C in 2100. Without deep and immediate cuts in emissions in all sectors, +1.5°C is out of reach. Solutions to halve emissions by 2030 already exist in all sectors. The evidence is clear: the time to act is now!